Church insurance helps protect churches, ministries, faith-based schools, and religious organizations from financial losses caused by property damage, lawsuits, employee claims, vehicle accidents, and other unexpected events. When purchasing church insurance, organizations should evaluate property values, liability exposures, ministry activities, and specialized coverage needs to ensure complete protection while controlling insurance costs.

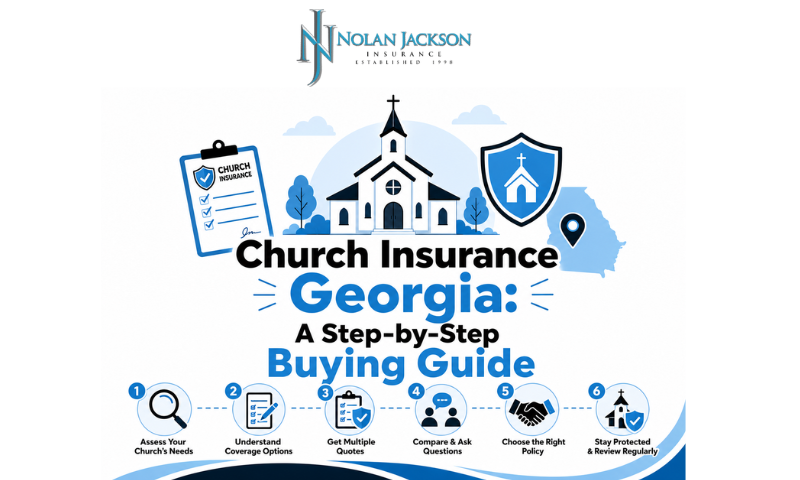

Purchasing church insurance coverage in Georgia requires more than simply comparing premiums. Churches must evaluate property risks, liability exposures, ministry programs, staff and volunteer activities, vehicles, schools, daycares, and business interruption needs. Working with a church insurance specialist helps ensure comprehensive protection tailored to the unique needs of faith-based organizations while avoiding costly coverage gaps.

Why Specialized Church Insurance Matters

Churches face unique risks that traditional commercial insurance policies may not fully address. A church is often much more than a worship facility. It may operate:

- Schools

- Daycare programs

- Community outreach ministries

- Counseling services

- Food pantries

- Mission programs

- Transportation services

- Recreational activities

Each of these activities creates additional liability exposures that require specialized protection.

Many church leaders discover coverage gaps only after a claim occurs. That’s why choosing the right Church Insurance Georgia policy is critical to protecting ministry operations, congregants, employees, volunteers, and physical assets.

Step 1: Assess Your Church’s Property Risks

Before requesting insurance quotes, create a complete inventory of church-owned assets.

Property Types to Evaluate

| Asset Type | Examples |

| Buildings | Sanctuaries, fellowship halls, offices |

| Equipment | Sound systems, computers, projectors |

| Furniture | Pews, chairs, tables |

| Religious Property | Altars, crosses, stained glass |

| Outdoor Assets | Signs, playgrounds, fences |

| Educational Facilities | Classrooms, libraries |

| Ministry Assets | Food pantry equipment, outreach supplies |

Common Property Risks in Georgia

Churches throughout Georgia face risks such as:

- Severe thunderstorms

- Wind damage

- Hail damage

- Fire losses

- Vandalism

- Theft

- Water damage

- Falling trees

A proper replacement cost valuation is essential. Many churches are significantly underinsured because property values have increased faster than policy limits.

Request a property valuation review every 2–3 years to ensure coverage keeps pace with construction costs.

Step 2: Evaluate Liability Exposures

Liability claims can be financially devastating for churches.

Even a small congregation can face substantial legal expenses if someone is injured on church property or alleges negligence.

General Liability Coverage Helps Protect Against:

- Slip-and-fall injuries

- Visitor accidents

- Property damage claims

- Event-related incidents

- Volunteer activities

- Medical payment expenses

Questions Church Leaders Should Ask

- Do we host community events?

- Do outside groups use our facilities?

- Do volunteers interact with children?

- Do we provide transportation?

- Do we offer counseling services?

The answers can significantly impact liability requirements.

Step 3: Consider Sexual Misconduct Liability Coverage

One of the most important coverages for modern churches is sexual misconduct liability insurance.

Unfortunately, allegations involving employees, clergy, volunteers, or ministry workers can result in substantial legal costs even when claims are unfounded.

Coverage may help with:

- Legal defense expenses

- Settlements

- Court judgments

- Investigation costs

Churches should also implement strong risk management practices, including:

- Background checks

- Volunteer screening

- Staff training

- Written safety procedures

- Two-adult supervision policies

Insurance and prevention should work together.

Step 4: Protect Church Leadership

Church leaders make important financial and operational decisions every day.

Those decisions can sometimes trigger legal disputes.

Directors & Officers (D&O) Coverage Helps Protect:

- Board members

- Executive pastors

- Church administrators

- Ministry leaders

- Finance committees

Claims may involve:

- Mismanagement allegations

- Financial decisions

- Governance disputes

- Employment decisions

- Regulatory issues

Without D&O coverage, church leaders may face significant personal financial exposure.

Step 5: Review Business Interruption Coverage

Many churches focus on protecting buildings but overlook the financial impact of operational disruptions.

Imagine a fire damages your sanctuary.

The church may need to:

- Rent temporary worship space

- Relocate offices

- Replace equipment

- Continue payroll expenses

- Maintain ministry programs

Business interruption insurance helps support ministry continuity during covered losses.

For many churches, preserving ministry operations is just as important as rebuilding physical property.

Step 6: Evaluate School and Daycare Exposures

Faith-based schools and daycare programs require specialized insurance considerations.

Additional risks often include:

- Student injuries

- Playground accidents

- Abuse allegations

- Educational liability

- Transportation risks

- Parent lawsuits

Coverage Often Needed

| Coverage Type | Purpose |

| General Liability | Visitor and student injuries |

| Professional Liability | Educational activities |

| Abuse & Molestation Coverage | Specialized protection |

| Property Insurance | Buildings and equipment |

| Commercial Auto | School transportation |

| Workers’ Compensation | Employee injuries |

Organizations operating schools or childcare programs should work with an insurance professional familiar with faith-based education risks.

Step 7: Review Vehicle and Transportation Risks

Many churches own:

- Vans

- Buses

- Passenger vehicles

- Ministry transportation vehicles

Vehicle-related claims can be among the most expensive losses churches experience.

Commercial auto coverage can help protect against:

- Bodily injury claims

- Property damage

- Collision losses

- Uninsured motorists

- Volunteer driver exposures

Churches should regularly review driver qualifications and vehicle maintenance procedures.

Step 8: Compare Insurance Providers Carefully

Not all insurance companies understand church operations.

When comparing options, focus on more than price.

Compare These Factors

| Evaluation Area | Why It Matters |

| Church Insurance Experience | Better understanding of ministry risks |

| Coverage Breadth | Fewer coverage gaps |

| Claims Handling | Faster recovery after losses |

| Risk Management Resources | Improved loss prevention |

| Policy Flexibility | Easier customization |

| Financial Strength | Ability to pay claims |

The lowest premium is not always the best value.

Step 9: Conduct an Annual Coverage Review

Churches evolve over time.

Insurance coverage should evolve as well.

Review policies annually if your organization experiences:

- Membership growth

- New building purchases

- Renovations

- School expansion

- New ministry programs

- Vehicle acquisitions

- Staff increases

Regular reviews help ensure your Church Insurance Georgia coverage continues to match your organization’s needs.

Common Mistakes Churches Make When Buying Insurance

Avoid these costly errors:

- Choosing coverage based solely on premium.

- Underinsuring buildings.

- Overlooking sexual misconduct liability.

- Ignoring business interruption coverage.

- Failing to insure ministry vehicles.

- Neglecting annual policy reviews.

- Working with agents who lack church insurance expertise.

A proactive approach can help reduce risk and strengthen long-term ministry stability.

Why Work with Nolan Jackson Insurance?

Churches need more than an insurance quote—they need guidance from professionals who understand the unique challenges facing faith-based organizations.

Nolan Jackson Insurance helps churches, ministries, schools, and religious nonprofits secure specialized coverage designed around their mission and operational needs.

Benefits of Working with Nolan Jackson Insurance

- Church-focused insurance expertise

- Customized coverage recommendations

- Competitive insurance options

- Assistance with risk management strategies

- Ongoing policy reviews

- Responsive claims support guidance

Whether your organization is a church plant, a growing congregation, a multi-campus ministry, or a faith-based school, the right insurance strategy can help safeguard your ministry for years to come.

Get a Church Insurance Review Today

If your renewal is approaching, your premiums have increased, or your ministry has expanded, now is the ideal time to review your coverage.

Contact Nolan Jackson Insurance today for a comprehensive church insurance assessment and discover how specialized protection can help secure your ministry’s future while controlling insurance costs.

Frequently Asked Questions

What does church insurance cover?

Church insurance typically covers property damage, liability claims, business interruption, leadership liability, and other ministry-related risks.

Is church insurance required in Georgia?

While not always legally required, lenders, landlords, and denominational organizations often require churches to maintain insurance coverage.

How much church insurance does a church need?

Coverage needs depend on property values, ministry activities, staffing, vehicles, schools, and liability exposures.

Do churches need sexual misconduct liability coverage?

Yes. This coverage is considered an essential part of a modern church insurance program due to the significant legal and financial risks involved.

How often should churches review insurance policies?

Most churches should review coverage annually or whenever major operational changes occur.